| |

| Home > Investment Stategy >Compounding |

|

| The Power of Compounding |

Compounding is the financial equivalent of a snowball rolling downhill. With each revolution, the snowball gets bigger because it picks up even more snow every time around. Compounding produces a snowball effect with money because the earnings each year contribute a little more to earnings the following year. As time passes, the earnings contribute more and more to the total value of an investment.

Growth of a monthly saving of Rs.1000 over a 30 year period

(Total savings: Rs.3.6 lacs)

|

|

| |

|

|

Assumed rate of return - 12% For illustrative purposes only

Growth on top of compounding

The basic principles of compounding apply to any mutual fund. Namely, reinvesting earnings (dividends and capital gains for non-money market funds) over time can lead to potentially large increases in value.

If a fund's share price rises, your initial investment grows independently of the effects of compounding. Although there's no guarantee that a fund's share price will increase, coupling this kind of growth potential with compounding has been an effective strategy for many long-term investors

The longer the period of your investment, the more you accumulate, because of the power of compounding... which is why it makes sense to start investing early.

|

| The secret is to start early (Example 1) |

| Meet Suresh and Manoj. Suresh invests Rs.5 OOO while Manoj invests twice as much. As illustrated in the table below, even though the amount invested by Suresh is half of what Manoj puts , his investment final amount is becomes twice as much as Manoj's, simply because he started earlier - a clear instance of the benefits of compounding. This is the power of compounding. |

| |

| Compounding Favours the Early Starter |

|

Suresh |

Manoj |

Investment Amount |

Rs.5,000 |

Rs.10,000 |

Investment Duration |

20 years |

10 years |

Final Amount |

Rs.81,833 |

Rs.40,456 |

|

| |

| Assumed annual rate of return - 15% with dividends and capital gains reinvested. For illustrative purposes only |

| The secret is to start early (Example 2)) |

| The key to building wealth is to start investing early and regularly. Regular investments, however small, can grow into a substantial amount of wealth over the long-term. Most of us tend to delay investing till the last moment. But the longer the delay, the more you'll need to put away in order to reach your goal. |

| |

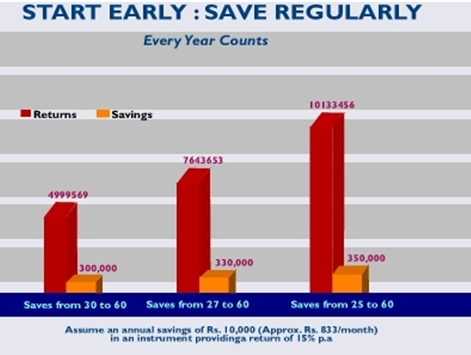

| The Cost of Delaying |

Sarvjeet, Sanjay and Sushil begin their careers together at the age of 25 but have different attitudes towards savings. Sarvjeet is a conservative spender and believes in saving. Sanjay and Sushil believe that with good careers ahead of them it does not really matter when they start saving.

Sarvjeet. Sarvjeet gets into the habit of saving regularly from day one. She successfully saves Rs.10,000 in the first year. She continues saving Rs.10,000 per year for 35 years till her retirement.

Sanjay. Sanjay gets married at the age of 27. With new responsibilities ahead of him, he gets into the habit of saving Rs.10,000 every year and continues saving Rs.10,000 per year for 33 years till his retirement.

Sushil. Sushil is the last one to start saving. He gets married and becomes a father at the age of 30. He, too, realises that he cannot delay his savings decision any more. He gets into the habit of saving Rs.10,000 every year and continues with this for 30 years till his retirement.

Sarvjeet began at age 25 and saved Rs.350,000; Sanjay began at age 27 and saved Rs.330,000 and Sushil began at age 30 and saved Rs.300,000.

|

|

| |

It seems quite obvious who saved more and who would have more wealth on their retirement. But consider this. If each of them got a compounded return of 15% per year on their savings, Sarvjeet would have over Rs.1 Crore, Sanjay approximately Rs.75 lacs and Sushil approximately Rs.49 lacs.

It does matter when you start saving… the earlier the better! |

| |

| Reinvest earnings and put your money to work |

You may have noticed that our example assumes that dividends and capital gains aren't taken in cash. Reinvesting your distributions increases the value of your portfolio which, in turn, increases the amount of interest earned each year.

Just like our snowball growing larger with each roll, the value of the investment increases by a greater amount each year as the earnings are put back in. As time passes, earnings generated by the reinvested interest can rival or surpass the earnings that come from the initial investment alone.

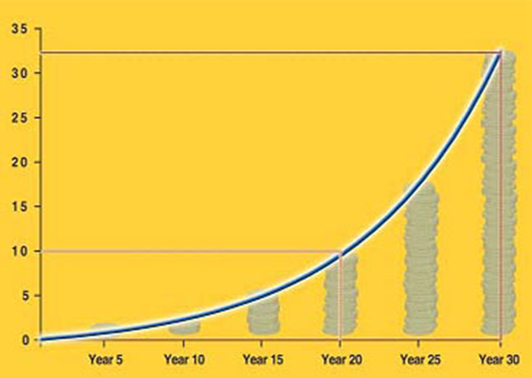

The longer you have, the better compounding works

Money starts multiplying, more towards the end, as can be seen in the following graph:

|

| Reinvest earnings and put your money to work |

You may have noticed that our example assumes that dividends and capital gains aren't taken in cash. Reinvesting your distributions increases the value of your portfolio which, in turn, increases the amount of interest earned each year.

Just like our snowball growing larger with each roll, the value of the investment increases by a greater amount each year as the earnings are put back in. As time passes, earnings generated by the reinvested interest can rival or surpass the earnings that come from the initial investment alone.

The longer you have, the better compounding works

Money starts multiplying, more towards the end, as can be seen in the following graph:

|

| |

| |

| |

|

| |

|